Imagine walking into your local supermarket, picking up essentials like bread, milk, and eggs, and paying for them later—not with a credit card, but with a Buy Now, Pay Later (BNPL) product. What was once a payment method for gadgets or clothes is now being used to pay for necessities.

This transition poses questions about consumerism, money health, and where the BNPL model fits into our new way of life. Let’s have a look at this new phenomenon and its implications…

The Rise of BNPL

BNPL solutions such as Klarna, Afterpay, and Affirm are the rage, allowing shoppers to pay in straightforward installments.

Starting with luxury or discretionary goods, it’s expanded to other product areas. The appeal? Immediate satisfaction without the initial expense. And people are now relying on this method even for food.

This trend deserves closer examination to understand how and why people are using it for everyday purchases.

Changing Consumer Behavior

Financial pressure, caused by inflation and stagnant salaries, has stretched budgets. To make up for it, consumers are using alternative payment methods to fill in the gaps.

BNPL offers a seemingly convenient answer, with deferred payments possible without the upfront burden of interest charges.

But convenience may come at an economic cost, especially when implemented on recurring expenses like grocery items. This practice is significant in grasping the broader financial effects.

Groceries on Credit

In a recent LendingTree survey, 25% of BNPL users employed the service to purchase groceries—a dramatic rise from 14% the previous year. This is a sign of a generational trend in BNPL use for essentials.

While it may provide short-term relief, reliance on instalment payments for commodities could create more fundamental financial distress in the future among consumers. The figures highlight the need to investigate how sustainable this practice is.

Demographics at a Glance

The same survey found that 64% of Gen Z consumers have used BNPL products, and a third utilized them to purchase grocery items. This evolving group means younger consumers are increasingly depending on BNPL for regular needs.

Potential motivations for the trend include limited access to mainstream credit, student loan debt, and economic uncertainty. Parsing these trends can provide insights into the money habits of nascent consumer segments.

The Debt Trap

While BNPL is easy, it’s also dangerous. LendingTree’s report says 41% of users have missed payments, up from 34% in the past year. Missed payments end in late fees, interest fees, and negative credit score effects.

For cash-strapped consumers, these consequences magnify the risk of falling into debt. It’s essential to think through the long-term effects of buying essentials with BNPL.

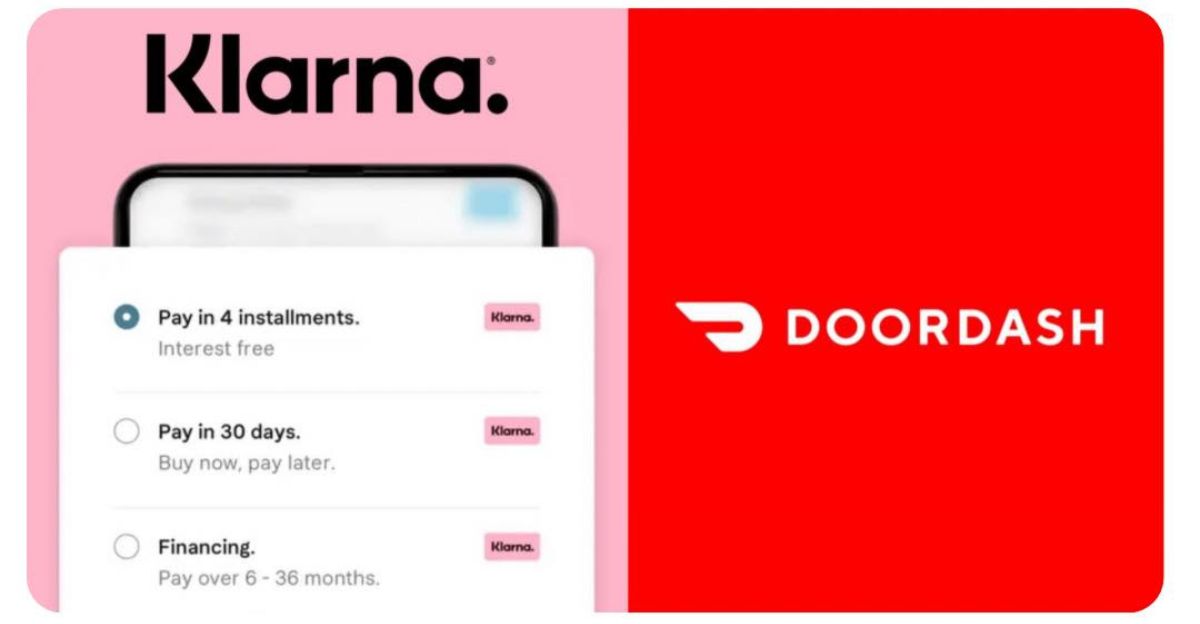

Business Response

In light of the demand, companies such as DoorDash have partnered with BNPL firms like Klarna to provide installment payments on food orders.

As much as it expands consumer choice, it also raises concerns about whether it promotes debt for food items.

Critics are concerned that such collaborations tend to favor short-term profit at the expense of consumers’ financial health. The ease-responsibility ratio is a contentious issue in the BNPL fraternity.

Regulation Issues

With increased use of BNPL, regulation becomes increasingly necessary. Some proponents argue that measures like credit checks, more transparent terms, and consumer education need to be implemented in an effort to forestall abuse.

Some nations have already begun contemplating regulatory strategies to govern BNPL providers. The aim is to keep consumers safe from harm without killing the advantages of flexible payment plans. Paying heed to these trends will be the key in unraveling the future of BNPL.

Consumer Awareness

Education is key to safely managing BNPL services. Consumers should be educated on the terms, possible charges, and late payment charges.

Finance education programs and transparency from BNPL providers can empower consumers to make informed choices. It all comes down to awareness and knowledge in using BNPL as a tool and not a trap.

Conclusion

Greater uptake of BNPL for food shopping is an indicator of deeper economic pressure and shifting consumer trends.

Although the items temporarily relieve pressure, they have the potential to trigger long-term financial tension when not used responsibly.

As the BNPL industry matures, all parties such as consumers, companies, and regulators have to work together to ensure that flexibility does not come at the expense of financial health. The future will require a balance between innovation and responsibility.

Discover more trending stories and Follow us to keep inspiration flowing to your feed!

Craving more home and lifestyle inspiration? Hit Follow to keep the creativity flowing, and let us know your thoughts in the comments below!